.webp)

For a deeper dive into Calyx Global’s recommendations for highly-rated cookstoves projects, download our Recipe for Success resource here.

Given the importance of improved cookstove (ICS) projects for emission reductions and contributions to the UN Sustainable Development Goals (SDGs), this blog aims to provide a shortened “recipe for success” for ICS projects to receive a high GHG rating by Calyx Global, and serves as a complement to our full paper. Here we outline the main risk factors for ICS projects and provide recommendations on mitigating these risks, based on our experience rating over 100 ICS projects.

Risk factors assessed by Calyx Global

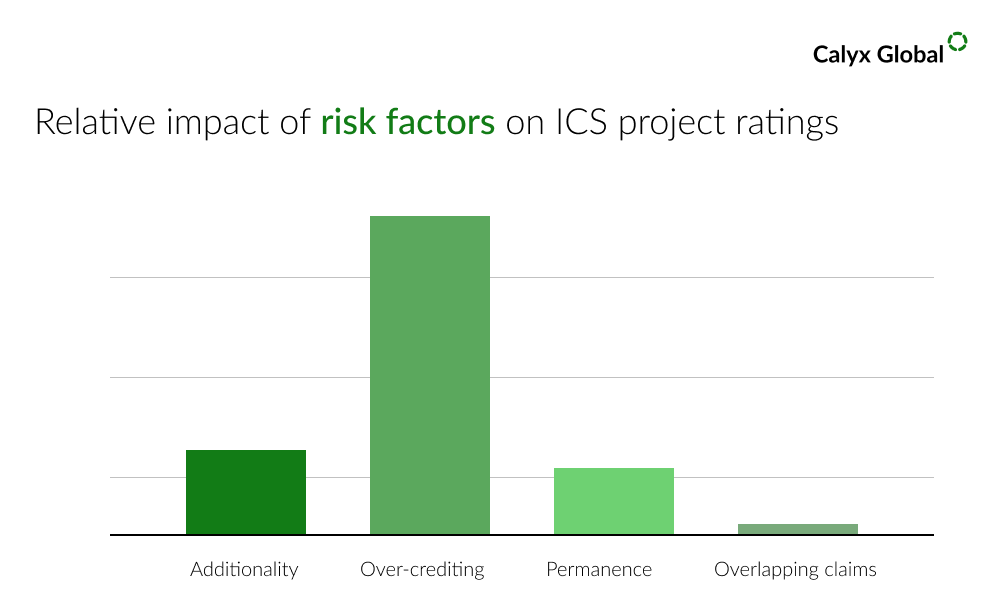

As outlined in our Improved Cookstove Ratings Framework, Calyx Global considers four risk factors when assessing improved cookstove projects: additionality, over-crediting, permanence and overlapping claims. Additionality has the greatest impact on all Calyx Global GHG ratings, and is a limiting factor (i.e. a final rating can not be higher than the risk of additionality). Cookstove projects, however, tend to have lower risks of non-additionality. By contrast, the risk of over-crediting tends to greatly impact the overall GHG integrity for ICS projects for several reasons, as explained in our recent ICS rating framework. The risk of non-permanence can also contribute significantly to the overall rating, although this impact tends to be lower than that of over-crediting. Finally, while there is sometimes a risk of overlapping claims, it rarely significantly impacts cookstove projects’ overall GHG rating.

Additionality:

Calyx Global evaluates the additionality of each project being rated and has found most ICS projects are likely to be additional, meaning they would not have occurred without carbon finance.

Nonetheless, ICS projects can have an increased risk of non-additionality if evidence suggests that carbon finance was unnecessary for the project to be implemented. Other factors contributing to the risk of non-additionality include the lack of demonstration that carbon finance was considered before the project’s start date (prior consideration) and the prevalence of improved cooking practices in the project area at the time of project implementation (common practice).

Over-crediting: Baseline, Project Emissions and Leakage

Over-crediting poses the highest risk to GHG integrity for ICS projects. Just over 50% of the ICS projects we have analyzed have a high risk of over-crediting. This means that their reported emission reductions are likely to be at least 80% greater than expected emission reductions when compared to independent, recent literature.

ICS projects claim emission reductions by lowering the demand for non-renewable fuel. To calculate emission reductions, a project must first define a “baseline scenario” and determine the amount and types of fuel(s) used in the baseline. A project then defines a “project scenario” and estimates fuel consumption after the deployment of the improved cookstoves. The emission reduction is the difference between these two scenarios. The potential for over-crediting lies in the difficulties of applying an accurate baseline and carefully designing the project to avoid overestimating emission reductions.

Calyx Global considers several quantitative and qualitative elements related to baseline and project emissions when assessing over-crediting. In addition, we assess leakage as a part of our over-crediting analysis to determine whether the project accounts for displaced emissions that occur outside of the project boundary due to the project’s activities. For more information on our rating process, see Calyx Global’s ICS Ratings Framework.

Permanence:

ICS projects have a risk of non-permanence since they receive credits for avoided emissions by conserving biomass that could be lost in the future due to other factors (e.g., fire, agricultural activities, land-use change). For ICS projects, the risk of non-permanence varies greatly depending on the country in which the project is implemented and whether the project utilized a charcoal or fuelwood stove.

The risk of non-permanence is not considered by any ICS methodology and is inherently difficult to model or predict. Nevertheless, Calyx Global believes that non-permanence should be considered when assessing a project’s GHG integrity. In the absence of methodology requirements, Calyx Global rates the risk of non-permanence for each project based on the available tree canopy reservoir and its estimated depletion rate in the area surrounding the project.

Overlapping claims:

Slightly more than half of the ICS projects reviewed by Calyx Global have overlapping boundaries, or are close to projects that claim to protect woody biomass — such as Reducing Emissions from Deforestation and Forest Degradation (REDD). Calyx Global assesses overlapping claims risk when there are other carbon projects that may claim to conserve the same biomass in the project region.

In our assessment, we make a distinction between the risk of overlapping claims for firewood projects, which typically involve traveling small distances to collect fuelwood; and charcoal projects, where the baseline fuel could have been produced and sourced much farther afield. As an example, some firewood ICS projects report operating across a country, and when there are also REDD projects in the country, this location distribution indicates a potential risk of overlapping claims, although at a lower risk level than if it were a charcoal project.

How to achieve higher ratings from Calyx Global

1. Provide robust documentation from the early stages of the projectBy providing clear and extensive information regarding the use and importance of carbon finance, projects can ensure that additionality is clearly demonstrated, potentially leading to a better rating by Calyx Global. Specifically, projects should include the following elements in publically available documentation:

- A clear demonstration that carbon revenue was considered before the project start date.

- Credible evidence that activities would not be financially attractive without carbon finance (e.g., investment analysis) and carbon revenue played a critical role in project implementation.

- An explicit statement on how carbon revenue is required to enable the project to be implemented.

- Identification of the project's target group (i.e. rural vs urban households/communities/institutions).

The risk of over-crediting for ICS projects is greatly impacted by baseline parameters used in calculating emission reductions (e.g., the fraction of non-renewable biomass - fNRB, baseline fuel consumption, wood-to-charcoal conversion factor, among others). Projects can mitigate the risk of over-crediting by applying conservative baseline parameters, even when it is not required at the methodology level.

Regarding fNRB, Calyx Global recommends that projects use the most recent, independently generated sub-national value (appropriate to the project scale) where possible, or conservative, independent national figures where they are available in peer-reviewed literature. If Tool 30 is used to determine fNRB, projects should apply a conservative approach to each parameter used as input in the Tool 30 equations.

Furthermore, as baseline conditions can shift during a project’s crediting period, Calyx Global recommends updating baseline parameters biennially to capture potential changes in the baseline scenario. Alternatively, projects can choose a shorter crediting period (e.g., five or seven-year periods), as baseline conditions are less likely to change in a short period.

3. Monitor the project scenario frequently, using the best available practices

An important aspect related to an ICS project’s over-crediting risk is the reliability and frequency of monitoring for project emissions. Many methodologies allow projects to monitor their performance via stove efficiency determined in a laboratory under controlled conditions. However, laboratory-based stove efficiency tests do not capture real-world cookstove performance, which tends to be worse in the field*. For more accurate measurements, projects should aim to use data loggers (i.e., stove use monitors), or measure project stove use by conducting field-based kitchen performance tests (KPTs).

Another key factor that builds confidence in the integrity of emission reductions is the monitoring of non-project stove use. Project households often continue to use their baseline technology after acquiring an improved stove, which can lead to unaccounted project emissions. Calyx Global recommends that ICS projects track baseline stove usage at least once every two years, with annual measurements preferred.

4. Address risks from leakage, non-permanence and overlapping claims

Leakage, non-permanence and overlapping claims are especially difficult for projects to address due to several factors, such as a lack of data and a lack of methodology-level guidance. For example, no existing methodology requires ICS projects to assess non-permanence directly, and ICS projects are not required to account for this risk. Similarly, the risk of overlapping claims is not addressed by any existing carbon standard, although the VCS recently released a draft methodology that includes guidance for overlapping claims which is not yet in effect.

In the absence of clear guidelines at the methodology level, Calyx Global encourages projects to adopt conservative values to mitigate risk across their GHG integrity profile. Furthermore, we recommend projects closely follow emerging guidance from carbon programs and the UNFCCC, as well as adopt best practices as they are being developed.

Regarding leakage, projects should thoroughly examine and track all potential sources of leakage (including space-heating, whenever relevant) and explain how leakage is quantified. If projects find no possibility for leakage, then this should be justified in publicly available documents. Projects that opt for a default leakage discount should aim to occasionally monitor leakage throughout the crediting period, to ensure that the discount is conservative and appropriate.

We note that simply fulfilling the requirements set by carbon crediting standards and methodologies does not guarantee a high rating in Calyx Global’s assessment of ICS projects. For more information on how carbon standards can “raise the bar” and how to address potential gaps in methodology requirements for the GHG integrity of ICS projects, see our full Recipe for Success resource, which outlines the latest best practices and specific ways to mitigate risk in the four risk categories assessed by Calyx Global.

In addition to this document, we have written a separate explainer that summarizes our rating framework, Calyx Global’s Improved Cookstove Ratings Framework. For buyers of credits interested in our ICS project ratings, reach out to us at @[email protected]

*E.g., Wathore, R., Mortimer, K. & Grieshop, A. P. In-Use Emissions and Estimated Impacts of Traditional, Natural- and Forced-Draft Cookstoves in Rural Malawi. Environ. Sci. Technol. 51, 1929–1938 (2017); Zhang, Z. et al. Systematic and conceptual errors in standards and protocols for thermal performance of biomass stoves. Renew. Sustain. Energy Rev. 72, 1343–1354 (2017); Gill-Wiehl, A., Price, T. & Kammen, D. M. What’s in a stove? A review of the user preferences in improved stove designs. Energy Res. Soc. Sci. 81, 102281 (2021); Muralidharan, V. et al. Field testing of alternative cookstove performance in a rural setting of western India. Int. J. Environ. Res. Public. Health 12, 1773–1787 (2015).

Acknowledgements: Calyx Global is solely responsible for the contents, but wishes to thank the following individuals for providing valuable review of this paper: Annelise Gill-Wiehl, Gustavo Andrade Reginato, Hilda Galt, Hayley Marshall, Keir Hamilton.

About the author

Calyx Global

This article includes insights and input from multiple experts in Calyx Global.

Get the latest delivered to your inbox

Sign up to our newsletter for the Calyx News and Insights updates.